Track Every Dollar Spent

Perhaps my most important goal this year is to track every dollar coming in and going out. How else can I get a good picture of how much I am saving and how much income I will ultimately need to replace. It is also the most effective way to see where I am wasting my money.

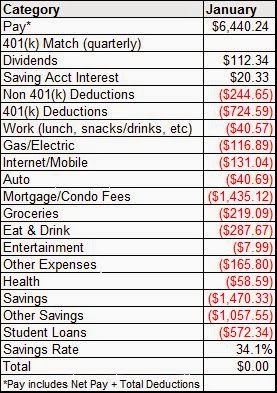

I am extremely happy with this start to the year. Please note the negative values for Savings and Other Savings are money I ‘spent’ to add to savings so those amounts increased my savings. The distinction between the two categories is that Savings is what I am putting towards my investments and/or my house down-payment fund. Other Savings is adding to accounts that will likely be spent down over time rather than invested. However, as these accounts do well, it allows me to add more to my regular Savings in future months. My savings rate is based only on the ‘Savings’ Category and does not include Other Savings. A 34.1% savings rate is very strong for me and starts my year on track for my 30%+ savings rate goal for 2014.

Looking forward the next several months, I will likely have a decent amount of wedding expenses coming my way. Other Expenses included annual jewelry insurance and a dry cleaning bill for my comforter which someone got sick on. Entertainment was my Netflix account while ‘Eat & Drink’ is eating out and having drinks. This is a category where I bleed money at times but my fiancee and I love to eat and drink. My spending at ‘Work’ is an area where I am really trying to cut back this year. January looked to be a good start but I picked up a $30 parking ticket at work which caused January to spike higher than it otherwise would have. Going forward, I expect Auto and Groceries spending to increase while spending on Health should decrease.

Dividends

As can be seen in the section above, I had $112.34 in dividends for the month of January. This was my first time eclipsing $100 in a month and represented an 86.8% increase vs. the previous (October). A big part of the increase was the timing of my dividends from DLR and PEP which shift their dividend from December to January (1/3/6/9 cycle). Currently, my March dividend should be similar size and I am hoping for a dividend increase to push March to a higher level (DLR?). My forward 12 month dividend income increased to $877.54, thanks to the ARCP dividend increase and the TGT purchase. I am increasing my forward target to $1500 by end of year as I now believe $1200 to be too conservative and I want my goals to be difficult so I have to push myself to attempt to reach them.

Backlog

As I mentioned, things have been hectic with wedding/honeymoon planning and the like. We are also launching a new product at work which has led to longer workweeks. As a result, I have a bit of a backlog in articles I want to write, including the start of what I hope to be a series of articles. There is one article (or small set of articles) I want to get out in February. As a preview, I want to highlight the biggest threat to KO, as I see it (their recent agreement with GMCR changes how I was going to attack this article which was unfortunate timing as I was really excited to go at it from the original direction), and how PEP may respond to KO’s recent GMCR move (hint: it’s not the conventional thinking to pair up with SODA).